Depreciation is defined as the systematic allocation of an asset’s cost over its useful life, reflecting wear, tear, and obsolescence. For founders, this accounting concept shapes reported earnings, tax bills, and how investors read your balance sheet. Understanding what depreciation means for founders is not optional. It directly affects how profitable your business looks on paper, how much tax you owe, and how much cash you actually keep. The IRS governs depreciation rules for U.S. businesses, and 2026 brought significant changes through the OBBBA law that every founder should know.

What does depreciation mean for founders?

Depreciation is a non-cash expense. It reduces your reported earnings on the income statement without touching your bank account. That distinction matters enormously for founders who confuse accounting profit with actual cash.

Say you buy a $60,000 piece of equipment. You do not expense the full $60,000 in year one under standard accounting rules. Instead, you spread that cost over the asset’s useful life, say five years, recognizing $12,000 per year. Your income statement shows lower profit each year, but your cash position only changed when you wrote the check.

Depreciation does not track market value. It reflects economic consumption over time, giving your financial statements consistent, predictable expense recognition. That consistency matters to investors and lenders who want to see expenses matched with the revenues an asset helps generate.

Founders who treat depreciation as a bookkeeping afterthought often miss its real power. It is a reporting outcome tied directly to your asset acquisition decisions, and it shapes both your tax strategy and your fundraising story.

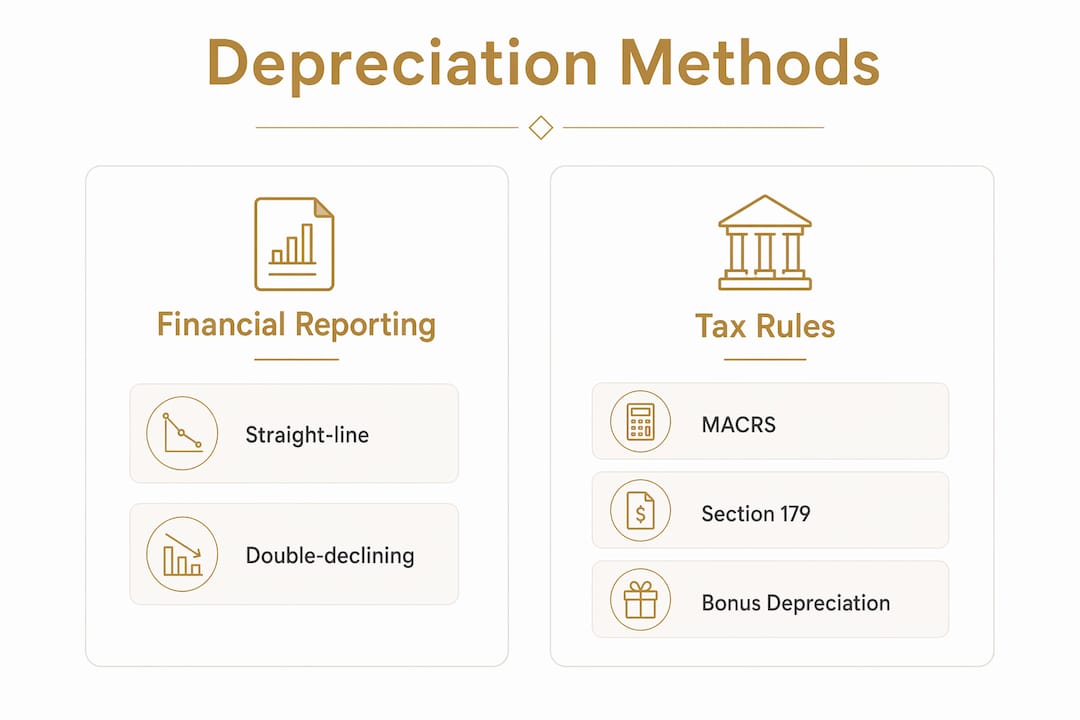

What are the common depreciation methods and how do they differ?

Three methods dominate startup financial reporting. Each produces a different expense pattern and a different picture of profitability.

Straight-line depreciation spreads cost evenly across the asset’s useful life. A $30,000 server with a five-year life generates $6,000 of depreciation expense every year. Simple, predictable, and favored for financial reporting.

Double-declining balance is an accelerated method. It front-loads expenses, recognizing more depreciation in early years and less later. That same $30,000 server might generate $12,000 of expense in year one and $7,200 in year two. Accelerated methods reduce taxable income faster, which can preserve cash early in a startup’s life.

MACRS (Modified Accelerated Cost Recovery System) is the IRS-mandated method for U.S. tax returns. It assigns assets to specific recovery periods and uses accelerated rates. Most founders use straight-line for their financial statements and MACRS for their tax returns, which is perfectly legal and common practice.

| Method | Expense pattern | Best use case |

|---|---|---|

| Straight-line | Equal each year | Financial reporting, investor clarity |

| Double-declining balance | Front-loaded | Early cash preservation |

| MACRS | IRS-prescribed | U.S. tax filings |

Selecting the correct depreciation method directly influences cash flow timing and how investors perceive your earnings. Founders who ignore this choice often cannot explain why their taxable income and operating performance diverge.

Pro Tip: If your startup is pre-profit, accelerated depreciation methods may create losses that carry forward. Time your asset purchases and method elections with your accountant before year-end, not after.

How do 2026 tax rules change depreciation strategy for founders?

Two provisions define the 2026 depreciation opportunity for founders: Section 179 and bonus depreciation. Both let you deduct asset costs faster than standard schedules. The differences between them determine which one you use first.

-

Bonus depreciation restored to 100%. The OBBBA law restored 100% first-year bonus depreciation for qualifying assets placed in service after january 19, 2025. That means you can deduct the full cost of a qualifying asset in the year you buy it.

-

Section 179 limit raised to $2.56 million. The Section 179 expense cap was adjusted for inflation to $2.56 million for tax year 2026. That covers virtually every early-stage startup’s annual equipment spend.

-

Section 179 is limited by taxable income. You cannot use Section 179 to create a net operating loss. If your startup is barely profitable, Section 179 deductions are capped at your taxable income for the year.

-

Bonus depreciation has no income limit. Bonus depreciation applies broadly and can create losses, making it more flexible for early-stage startups with uncertain profits. Those losses can carry forward to offset future income.

-

Sequence matters. Apply Section 179 first to assets where you want selective control. Then apply bonus depreciation to remaining qualifying assets. This order gives you the most flexibility and avoids wasting deductions.

The practical implication: a founder who buys $150,000 of qualifying equipment in 2026 can potentially deduct the entire amount in year one. That deduction lowers taxable income immediately, preserving cash for growth.

Pro Tip: Bonus depreciation is the more powerful tool when your startup runs at a loss or near breakeven. Section 179 is better when you have taxable income to offset and want to choose which assets to expense.

Why does depreciation matter beyond accounting?

Depreciation’s real value to founders lives in three places: cash flow, valuation metrics, and balance sheet accuracy. Most founders only think about the first one.

Cash flow. Depreciation reduces your tax bill without reducing your cash. A $50,000 deduction at a 25% effective tax rate saves $12,500 in cash taxes. That $12,500 stays in your business. Accelerated tax deductions can defer or reduce tax liabilities, freeing up working capital for inventory, marketing, or hiring.

Valuation metrics. Investors often look at EBITDA (earnings before interest, taxes, depreciation, and amortization) to assess operating performance. EBITDA adds depreciation back to net income, so high depreciation does not penalize your valuation multiple in investor conversations. Understanding this distinction helps you present your financials confidently.

Balance sheet accuracy. Every asset you own sits on your balance sheet at its original cost minus accumulated depreciation. That net figure is called book value. Proper fixed asset management prevents “ghost assets,” which are fully depreciated or disposed assets that still appear on your books. Ghost assets inflate your balance sheet and create reconciliation problems during due diligence.

“High depreciation expenses indicate significant asset consumption. For startups, that signal is critical for understanding both financial health and valuation.”: Invest In Mood

Founders raising capital or preparing for an exit need clean fixed asset records. Investors and acquirers will scrutinize your balance sheet. Inaccurate asset values create doubt about the quality of your entire financial reporting. This is one of the most common founder financial blind spots that surfaces during due diligence.

How should founders practically manage depreciation and fixed assets?

Depreciation management is not a year-end scramble. It is a year-round discipline. Here is how to build it into your operations.

-

Build a fixed asset register. Record every asset above your capitalization threshold (typically $2,500 or more). Include purchase date, cost, useful life, depreciation method, and accumulated depreciation. A spreadsheet works at the start. Accounting software like QuickBooks or Xero has fixed asset modules that automate the math.

-

Choose methods intentionally. Decide upfront whether you are using straight-line for financial reporting and MACRS for taxes. Document your elections. Changing methods mid-stream creates complexity and IRS scrutiny.

-

Track additions, disposals, and retirements. When you sell or retire an asset, remove it from your register immediately. Maintaining clean fixed asset policies year-round avoids reconciliation problems and keeps your tax filings accurate.

-

Work with your accountant before major purchases. Timing matters. An asset placed in service on december 31 qualifies for a full year of MACRS depreciation in many cases. An asset placed in service on january 1 of the following year delays your deduction by 12 months.

-

Integrate depreciation into your financial dashboard. Your monthly reporting should show depreciation expense by asset category. That visibility helps you spot when asset consumption is outpacing replacement, which is an early warning sign for capital planning.

Pro Tip: Organize asset purchases strategically during the fiscal year. Buying equipment in Q4 can accelerate deductions into the current tax year. Buying in Q1 spreads the benefit forward. Neither is wrong, but the choice should be deliberate, not accidental.

Understanding financial clarity and growth planning requires treating depreciation as a live input to your decisions, not a line item your accountant handles once a year.

Key Takeaways

Depreciation is a non-cash expense that reduces taxable income without reducing cash, making it one of the most underused financial tools available to founders.

| Point | Details |

|---|---|

| Depreciation definition | It allocates asset cost over useful life, reducing reported earnings without affecting cash. |

| Method selection matters | Straight-line suits financial reporting; MACRS and accelerated methods reduce taxes faster. |

| 2026 tax opportunity | OBBBA restored 100% bonus depreciation; Section 179 limit is now $2.56 million for 2026. |

| Cash flow impact | Tax deductions from depreciation preserve cash by lowering your actual tax bill each year. |

| Clean asset records | A fixed asset register prevents ghost assets and protects your balance sheet during due diligence. |

Depreciation as a strategic tool, not a tax afterthought

The second mistake is using Section 179 when bonus depreciation would have been more powerful. Section 179 is capped by taxable income. If your startup is running at a loss or near breakeven, Section 179 deductions get wasted. Bonus depreciation can create a net operating loss that carries forward, giving you a future tax shield when you actually start generating profit. The sequencing decision alone can be worth tens of thousands of dollars.

Do not buy assets purely for the deduction. The investment has to stand on its own business merits. But when the investment makes sense, structuring the depreciation correctly is free money left on the table if you ignore it.

How Commerce Catalyst helps founders get financial clarity

Founders who understand depreciation conceptually still struggle to apply it consistently across a growing business. The details compound fast: method elections, asset registers, tax timing, and investor presentation all require coordination.

Commerce Catalyst works directly with consumer brand founders to translate financial complexity into clear decisions. The DTC Financial Health Assessment evaluates your full financial picture, including fixed asset management and depreciation strategy, and identifies where you are leaving cash on the table. For founders who need ongoing financial leadership, the Fractional CFO service provides expert guidance on tax timing, method elections, and balance sheet accuracy without the cost of a full-time hire. Both services are built for founders who want to run a tighter, more profitable business.

FAQ

What is the simplest depreciation definition for founders?

Depreciation is the process of spreading an asset’s purchase cost across its useful life as an annual expense. It reduces reported profit without reducing your cash balance.

How does depreciation affect startup cash flow?

Depreciation itself does not reduce cash, but the tax deductions it generates do lower your tax bill. That tax savings preserves cash that stays in your business.

What is the difference between Section 179 and bonus depreciation in 2026?

Section 179 is capped by your taxable income and cannot create a loss. Bonus depreciation has no income limit and can generate a net operating loss that carries forward to future tax years.

Which depreciation method should founders use?

Most founders use straight-line depreciation for financial reporting and MACRS for their tax returns. The right choice depends on your profit position and cash flow needs, so consult your accountant before electing a method.

What is a ghost asset and why does it matter?

A ghost asset is a fully depreciated or disposed item that still appears on your balance sheet. Ghost assets inflate reported asset values and create problems during investor due diligence or an acquisition process.