Growth and profitability are the two most contested priorities in any business strategy conversation, and choosing between them is rarely as binary as it sounds. The real discipline, known formally as profitable growth management, is learning to improve both simultaneously rather than treating them as opposites. 91% of entrepreneurs now view disciplined growth with a clear route to profitability as more important than rapid market expansion. That shift reflects a hard truth: growth without profit burns cash, and profit without growth stagnates value. This guide gives you the frameworks, metrics, and execution tactics to make that call with confidence.

How to choose between growth and profitability

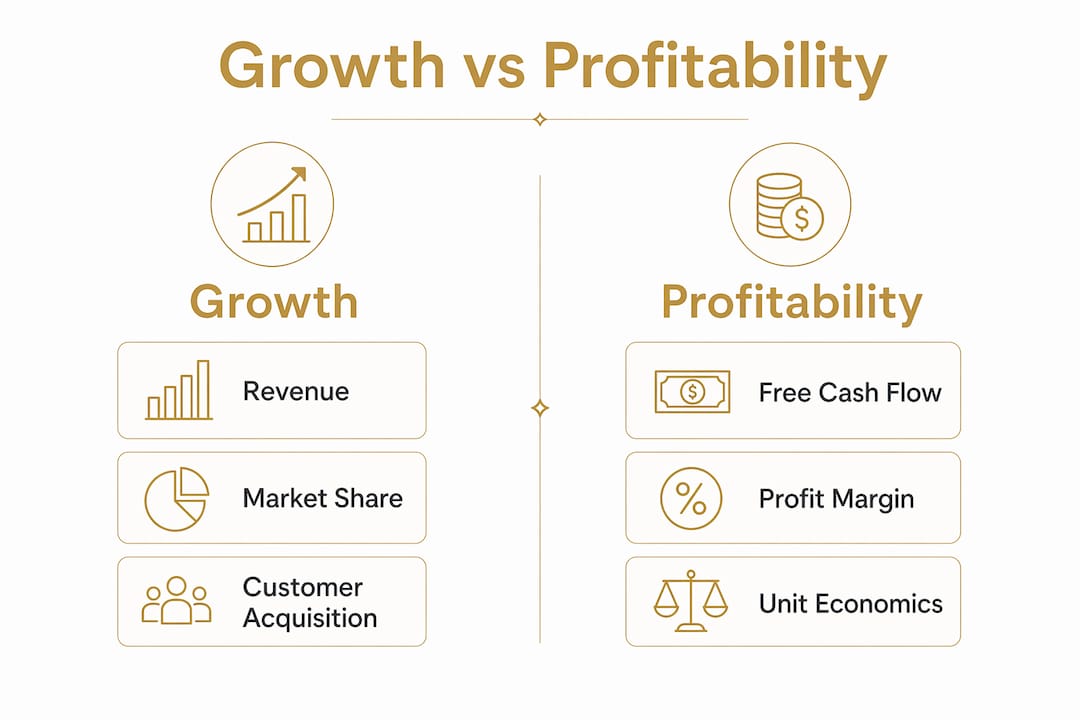

The challenge is not picking a winner. It is understanding which one your business needs right now and what constraints govern that choice. Growth drives future enterprise value by expanding market share, customer base, and revenue potential. Profitability fuels present viability by generating the cash needed to fund operations, service debt, and reward investors. Neither alone guarantees success.

The tension becomes acute when capital is scarce. 59% of founders report increasing constraints on growth capital compared to the previous year. That means the cost of chasing growth without a profit plan is higher than it has ever been. A SaaS startup burning $2M per month to acquire customers at a 24-month payback period is making a bet that future funding will arrive before the runway ends. That bet is getting harder to win.

Three structural forces make this decision difficult for most leaders:

- Capital allocation pressure. Every dollar spent on growth marketing, headcount, or inventory is a dollar not flowing to the bottom line. The tradeoff is immediate and visible.

- Execution risk. Growth investments take time to compound. Profitability improvements show up in the next quarter. Boards and investors often reward the faster signal.

- Measurement confusion. Many companies track accounting profit rather than free cash flow, which obscures the real cost of growth investments and leads to poor capital decisions.

Pro Tip: Before any strategic planning session, separate your maintenance cash costs from your growth investment cash. Separating these two buckets gives you a cleaner view of what growth is actually costing you and whether it is generating a return.

What frameworks and metrics actually help you decide?

The most widely used benchmark for balancing growth and profitability in high-growth companies is the Rule of 40. The Rule of 40 combines annual revenue growth rate and free cash flow margin into a single score, with 40 or higher considered healthy. A company growing at 30% with a 10% free cash flow margin scores exactly 40. One growing at 50% but losing 15% scores 35 and needs to course-correct.

Investors and boards use this score as a quick signal of capital efficiency. Rule of 40 scores communicate growth-plus-profitability efficiency directly to VCs and boards, which is why it has become the default language in SaaS funding conversations. Consumer brands and DTC operators can apply the same logic even if their metrics look different.

Beyond the Rule of 40, two other frameworks deserve attention:

| Framework | What it measures | Best used for |

|---|---|---|

| Rule of 40 | Revenue growth rate + free cash flow margin | SaaS, subscription, and high-growth DTC brands |

| Commercial excellence | Pricing discipline, customer segmentation, and revenue quality | B2B and consumer brands scaling revenue profitably |

| Free cash flow focus | Cash generated after maintenance and growth capex | Capital-intensive businesses and brands managing debt |

Commercial excellence is the framework most underused by consumer brand founders. Companies that prioritize commercial excellence initiatives earn 1.7x total shareholder return versus peers, according to Bain. The mechanism is clear: better pricing, smarter customer segmentation, and tighter revenue quality reduce the cost of each dollar of growth.

Pro Tip: Free cash flow margin is more defensible than EBITDA margin in modern valuations. Free cash flow margin strips out accounting adjustments and shows what the business actually generates. Use it as your primary profitability metric, not net income.

How to execute a growth-profitability balance in practice

Frameworks are only useful if you can act on them. Here is a practical sequence for business leaders who want to move from theory to execution.

1. Establish unit economics guardrails first. Before approving any growth investment, define the minimum acceptable customer acquisition cost (CAC) payback period and gross margin floor. Growth investment managed within unit economics guardrails produces durable financial health. Without these guardrails, growth spending becomes revenue chasing with no accountability.

2. Segment your customers and products by profit contribution. Not all revenue is equal. Profitable growth requires identifying where money is being lost at the SKU and customer level. A DTC brand selling 200 SKUs often finds that 20% of those SKUs generate 80% of the profit and another 30% actively destroy margin through returns, discounting, and fulfillment costs.

3. improve pricing before cutting costs. Most founders reach for cost reduction when margins compress. Pricing is a faster lever. Reducing discounting by 5 percentage points on a $10M revenue base adds $500K to gross profit without touching the cost structure. Review your pricing against value delivered, not against competitors.

4. Use AI and automation to improve revenue per employee. Scaling headcount inefficiently traps margin expansion. AI tools that automate customer service, inventory forecasting, and performance marketing analysis let you grow revenue without proportional headcount growth. This is one of the six operating levers that can shift a Rule of 40 score by one to six points within a year.

5. Track net revenue retention as a growth quality signal. Net revenue retention above 120% means your existing customers are spending more over time, which reduces reliance on expensive new customer acquisition. Expansion revenue from existing customers costs a fraction of new logo acquisition and improves both growth rate and profitability simultaneously.

The table below shows how these levers interact with your Rule of 40 score:

| Lever | Impact on growth rate | Impact on profit margin |

|---|---|---|

| Pricing improvement | Neutral to positive | +2 to +5 points |

| AI-driven CAC reduction | Positive | +1 to +3 points |

| NRR improvement | Positive | +2 to +4 points |

| Headcount efficiency | Neutral | +1 to +3 points |

| SKU rationalization | Neutral to negative | +2 to +6 points |

What are the most common pitfalls in growth vs profitability strategy?

Most strategic failures in this area come from a small set of recurring mistakes. Recognizing them early saves significant time and capital.

- Confusing accounting profit with cash reality. Net income can look healthy while free cash flow is negative due to inventory buildup, deferred revenue, or aggressive depreciation schedules. Always reconcile the two before making capital allocation decisions.

- Overinvesting in growth without unit economics discipline. Spending $3 to acquire a customer worth $2 is not a growth strategy. It is a liquidation event in slow motion. Define your payback period ceiling and enforce it.

- Ignoring the source of growth. New logo acquisition and upsell revenue have very different cost profiles. A company growing 40% through upsells is in a fundamentally stronger position than one growing 40% through discounted new customer acquisition. Track both separately.

- Failing to manage profit leaks at the SKU or customer level. Aggregate margin numbers hide the damage done by loss-making products or high-churn customer segments. Granular profit pool analysis, as Bain recommends, is the only way to see where value is actually being created or destroyed.

- Neglecting free cash flow as the primary scorecard. Tracking free cash flow rather than net income aligns strategy execution, capital allocation, and debt management into a single coherent picture. Companies that manage to accounting profit alone routinely run out of cash while reporting positive earnings.

The pattern behind most of these mistakes is the same: leaders improve for the metric that is easiest to report rather than the one that most accurately reflects business health. Fixing that starts with choosing the right scorecard.

Key takeaways

Balancing growth and profitability requires unit economics discipline, granular profit pool analysis, and free cash flow as your primary scorecard.

| Point | Details |

|---|---|

| Rule of 40 as your benchmark | Combine revenue growth rate and free cash flow margin; a score of 40 or higher signals capital efficiency. |

| Unit economics before growth spend | Set CAC payback and gross margin floors before approving any growth investment. |

| Segment by profit contribution | Identify which SKUs and customers generate profit and which destroy it before scaling. |

| Free cash flow over net income | Use free cash flow margin as your primary profitability metric to avoid misleading accounting signals. |

| NRR as a growth quality signal | Net revenue retention above 120% reduces CAC dependency and improves both growth and margin simultaneously. |

How Commerce Catalyst helps you find the right balance

Knowing the frameworks is one thing. Applying them to your specific brand, cost structure, and growth stage is another. Commerce Catalyst works directly with consumer brand founders to translate these financial realities into decisions you can act on this quarter.

The DTC Financial Health Assessment gives you a clear picture of where your growth spending is generating returns and where it is leaking margin. For founders who need ongoing financial leadership, the fractional CFO service provides CFO-level oversight without the full-time cost, covering free cash flow management, pricing strategy, and capital allocation. If you want to start with a fast diagnostic, the DTC Operator Diagnostic identifies your highest-priority constraints in a single session. You can also review the profitability roadmap methodology to understand the process before committing.

FAQ

What is the Rule of 40 and why does it matter?

The Rule of 40 is a benchmark that combines revenue growth rate and profit margin into a single score, with 40 or higher indicating a healthy balance between growth and profitability. Investors and boards use it to assess capital efficiency without having to choose between growth and profit as separate priorities.

Is growth more important than profitability for early-stage companies?

Growth typically takes priority in early stages when market share and product-market fit are the primary objectives, but it must operate within unit economics guardrails. Without a defined path to profitability, early-stage growth consumes capital faster than most funding environments can replenish it.

How do I know if my growth is profitable?

Track net revenue retention, CAC payback period, and gross margin by customer segment and SKU. If your NRR exceeds 120% and your CAC payback is under 12 months, your growth is generating compounding returns rather than just consuming capital.

What is the difference between free cash flow and accounting profit?

Accounting profit includes non-cash items like depreciation and can be positive while the business is cash-negative due to inventory or receivables growth. Free cash flow reflects actual cash generated after operating and capital expenditures, making it the more reliable metric for evaluating financial health and growth sustainability.

How can consumer brands apply the Rule of 40?

Consumer brands can adapt the Rule of 40 by substituting revenue growth rate and contribution margin or free cash flow margin as their two inputs. Reviewing industry benchmarks for CAC, margins, and LTV gives you the context needed to set realistic targets for your category.