A business moat, formally called an economic moat, is defined as a durable structural advantage that allows a company to sustain returns on invested capital above its cost of capital for 10 to 20 or more years. Warren Buffett coined the term, and it remains the single most important qualitative factor investors use to separate great businesses from average ones. Companies like Coca-Cola and Microsoft have held dominant market positions for decades precisely because their moats make competition economically unattractive. For investors and analysts, understanding what is a business moat means knowing which companies can protect their profits long after the initial growth story fades.

What is a business moat investors should recognize?

The business moat definition starts with one question: what stops a well-funded competitor from copying this company’s success? If the answer is “not much,” there is no moat. If the answer involves structural barriers that would take years and billions of dollars to replicate, you are looking at a real economic moat.

The term entered mainstream investing through Warren Buffett’s annual letters to Berkshire Hathaway shareholders. Buffett described the ideal business as a castle surrounded by a wide, deep moat. The castle is the business. The moat is what keeps rivals from taking it. Morningstar later built an entire equity research framework around this concept, assigning wide moat, narrow moat, or no moat ratings to thousands of publicly traded companies.

From an investor perspective on moats, the core insight is this: moats lower the risk profile of a company’s future cash flows. A business without a moat faces constant pressure on margins and market share. A business with a wide moat can raise prices, retain customers, and generate excess returns for decades. That difference in predictability is worth a significant premium in any valuation model.

What are the five primary types of business moats?

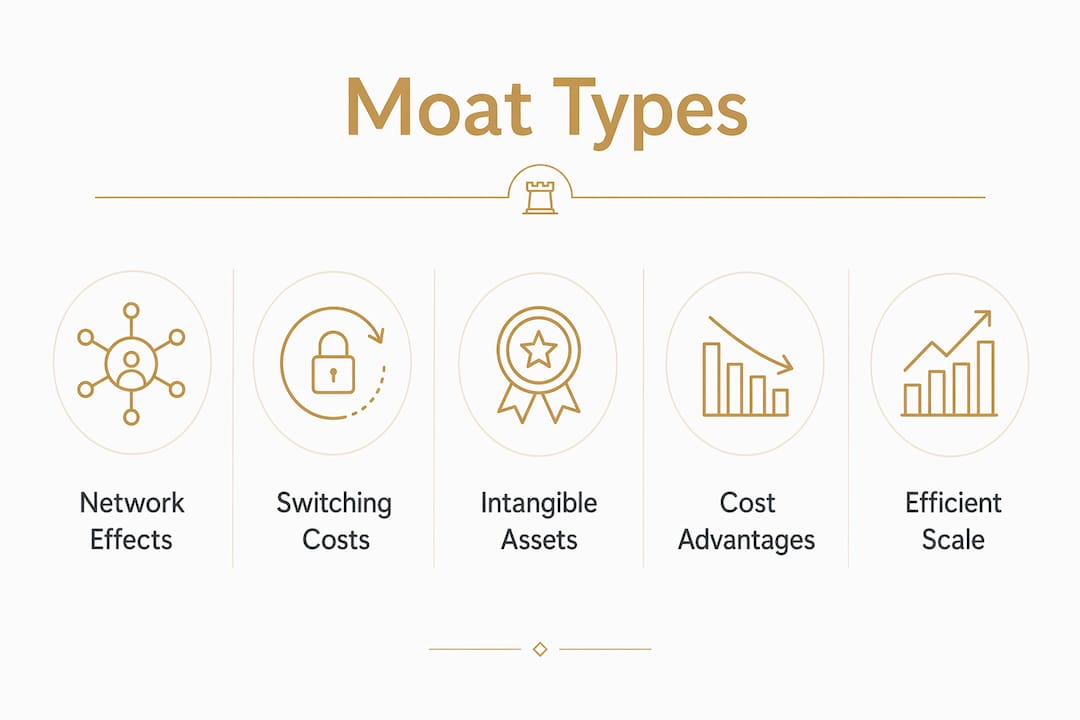

Five primary moat types define how companies build structural competitive advantages. Each one makes it uneconomical for rivals to replicate the business model at scale.

| Moat Type | How It Works | Real-World Example |

|---|---|---|

| Network Effects | Value grows as the user base expands | Visa, Meta |

| Switching Costs | Customers face high costs or friction to leave | Microsoft Office, Salesforce |

| Intangible Assets | Brands, patents, and licenses create exclusivity | Coca-Cola, pharmaceutical firms |

| Cost Advantages | Scale or geography enables lower unit costs | Walmart, Costco |

| Efficient Scale | Small markets support only one or two players | Regional utilities, pipelines |

Network effects are among the most powerful moat types. Visa’s payment network becomes more valuable every time a new merchant or cardholder joins. A competitor cannot replicate that network overnight regardless of capital available.

Switching costs are subtler but equally durable. Salesforce customers build entire sales operations around its CRM platform. Migrating to a competitor means retraining staff, rebuilding integrations, and accepting months of productivity loss. That friction is the moat.

Intangible assets include patents, regulatory licenses, and brand equity with proven pricing power. A pharmaceutical company holding a 20-year drug patent faces zero direct competition on that molecule. Coca-Cola’s brand commands shelf space and consumer loyalty that no amount of advertising spend can quickly replicate.

Cost advantages work at scale. Walmart’s supply chain and distribution infrastructure allow it to price below competitors while maintaining margins. Costco’s membership model funds operations at near-zero retail margins, making it structurally impossible for smaller rivals to match prices.

Efficient scale applies to industries where the market is too small to support more than one or two profitable players. A regional natural gas pipeline serving a specific geography has a natural monopoly. A second pipeline would destroy returns for both operators.

Pro Tip: When evaluating moat type, ask whether the advantage compounds over time. Network effects and switching costs tend to get stronger as the business grows. Cost advantages can erode if a competitor achieves similar scale.

How can investors identify a true economic moat?

Identifying a real moat requires both quantitative and qualitative analysis. Narratives about brand strength or product quality are not enough. The financial statements must confirm what the story claims.

The clearest financial signature of a moat is ROIC consistently above 20% for five or more years. Return on invested capital measures how efficiently a company generates profit from the capital it deploys. When ROIC stays well above the cost of capital for years, it signals that competitors have not been able to erode those returns. That persistence is the moat showing up in the numbers.

Stable or rising gross margins during economic downturns are another strong signal. A company with pricing power does not need to discount to retain customers. Subscription businesses with customer retention above 90% demonstrate that switching costs or product lock-in are real, not assumed.

Pat Dorsey, former director of equity research at Morningstar and author of The Little Book That Builds Wealth, built his career around this exact framework. His work distinguishes between companies with genuine structural advantages and those benefiting from temporary tailwinds. Morningstar’s MOAT ETF applies this framework systematically across public equities.

Red flags that suggest no durable moat:

- ROIC declining toward the cost of capital over a 3–5 year period

- Gross margins compressing in a growing market

- Customer churn above 15% annually in subscription models

- Competitive wins driven primarily by price discounting

- Market share gains tied to a single product cycle rather than platform depth

- Leadership changes that correlate with performance shifts

Pro Tip: Run a 10-year ROIC trend before accepting any moat narrative. A single great year proves nothing. Ten consecutive years of above-cost-of-capital returns is hard to fake.

Why do business moats matter for valuation and strategy?

Moats directly change how analysts model a company’s future value. In a discounted cash flow model, the terminal value often represents 60–80% of the total estimated value. Wide moats justify higher terminal values because analysts can reasonably assume excess returns will persist for 20 or more years rather than mean-reverting within a decade.

This is why wide-moat companies like Coca-Cola and Microsoft trade at premium multiples relative to their near-term earnings. The market is pricing in the durability of their competitive position, not just next year’s cash flow. Without that moat, the same earnings would justify a much lower multiple.

From a portfolio construction standpoint, moat analysis shifts investing from speculation to probability. Consider the difference between these two investment postures:

- Buying a high-growth company with no structural advantage and hoping the growth continues long enough to justify the price paid.

- Buying a wide-moat company at a fair price and holding it for 15 years while the competitive position compounds.

The second approach does not require perfect timing or market prediction. It requires accurate moat identification and valuation discipline.

“The key to investing is not assessing how much an industry is going to affect society, or how much it will grow, but rather determining the competitive advantage of any given company and, above all, the durability of that advantage.”: Warren Buffett

Operators and CEOs apply the same logic internally. Moat building is strategic capital allocation, not just a financial metric. Amazon spent years sacrificing near-term profits to build logistics infrastructure, AWS, and Prime membership. Each investment widened the moat. Investors who understood that framework held through the volatility and were rewarded.

What are the most common misconceptions about business moats?

The most expensive mistake investors make is confusing a great product with a structural advantage. A moat must be structural and durable, not a reflection of current product quality or management talent. Products get copied. Management teams change. Neither qualifies as a moat.

First-mover status is another common false moat. Being first to market creates a temporary lead, not a permanent one. MySpace was first. Facebook won. The moat belongs to the company that builds structural barriers after the initial market entry, not the one that arrived first.

A strong brand is frequently cited as a moat, but brand alone is insufficient without financial proof. A brand that cannot support pricing power above competitors, or that requires constant marketing spend to maintain share, is not a moat. It is a marketing expense.

Common mistakes investors make when assessing moats:

- Accepting management’s own moat narrative without verifying it in the financials

- Treating market share as a proxy for moat strength without examining margin trends

- Ignoring technological shifts that could make current advantages obsolete

- Assuming regulatory protection is permanent rather than subject to policy change

- Overweighting brand recognition in consumer categories with low switching costs

Warren Buffett himself has noted that technology and consumer preferences can widen or erode moats in ways that are difficult to predict. The newspaper industry once had powerful local advertising moats. Digital platforms eliminated them within 15 years.

How do investors apply moat analysis in practice?

Moat analysis works best when it integrates quantitative financial review with qualitative competitive research. Start with the financial statements. Pull 10 years of ROIC, gross margin, and free cash flow data. Look for consistency and direction, not just absolute levels.

Then layer in qualitative research. Read customer reviews, competitor filings, and industry analyst reports. Ask whether the company’s advantage comes from a structural source or from execution alone. Execution advantages are real but not durable. Structural advantages persist even when execution slips.

For investors building a moat-focused portfolio, the VanEck Morningstar Wide Moat ETF (ticker: MOAT) provides direct exposure to companies Morningstar rates as wide moat at attractive valuations. It applies the framework systematically and rebalances quarterly. Studying its holdings is itself an education in applied moat analysis.

Scenario planning adds another layer of rigor. Ask what would have to be true for this moat to erode within 10 years. Identify the specific technological, regulatory, or behavioral shifts that could undermine the advantage. If those scenarios are plausible and near-term, the moat is narrower than it appears.

For founders and operators, moat analysis is not just an investor tool. Understanding how to position your brand for structural advantage changes how you allocate capital, price products, and build customer relationships. The same logic that guides Buffett’s stock picks should guide every major strategic decision inside a growing business.

Pro Tip: Pair moat analysis with a review of founder financial blind spots to catch the gaps between what a business claims as its advantage and what the numbers actually support.

Key takeaways

A business moat is the single most reliable predictor of long-term investment returns because it determines whether a company can defend its profitability against competition for decades, not just quarters.

| Point | Details |

|---|---|

| Moat definition | An economic moat is a structural advantage sustaining ROIC above cost of capital for 10–20 years. |

| Five moat types | Network effects, switching costs, intangible assets, cost advantages, and efficient scale each block competition differently. |

| Financial proof required | Consistent ROIC above 20% for five or more years is the clearest quantitative signal of a real moat. |

| Valuation impact | Wide-moat companies justify higher terminal values in DCF models due to expected long-term excess returns. |

| Moats are not permanent | Technology, regulation, and consumer behavior can erode any moat; ongoing reassessment is required. |

How Commerce Catalyst helps you find and strengthen your moat

Understanding your competitive advantage on paper is one thing. Seeing it confirmed or challenged in your actual financial data is another. Commerce Catalyst works directly with consumer brand founders to surface the financial signatures of real structural advantages, or identify where the numbers tell a different story than the narrative.

The DTC Financial Health Assessment examines your margins, ROIC trends, customer retention, and cost structure to determine whether your business has the financial profile of a durable competitive position. The Operator Diagnostic goes deeper into operational strengths and where capital allocation is either building or eroding your advantage. If you are preparing for investment or planning your next growth phase, these assessments give you the evidence base to make that case with confidence.

FAQ

What is a business moat in simple terms?

A business moat is a structural competitive advantage that protects a company’s profits and market share from rivals over the long term. The term comes from Warren Buffett, who used the castle-and-moat analogy to describe businesses that competitors cannot easily attack.

What are the five types of economic moats?

The five primary moat types are network effects, switching costs, intangible assets, cost advantages, and efficient scale. Each one creates a different structural barrier that makes it uneconomical for competitors to replicate the business model.

How do investors identify a real moat versus a narrative?

Real moats show up in the financial statements as ROIC consistently above 20% for five or more years, stable gross margins, and high customer retention. A compelling story without those financial signatures is not a moat.

Why do wide-moat companies trade at premium valuations?

Wide-moat companies justify higher multiples because their competitive advantages support persistent excess returns for 20 or more years. That durability increases terminal value assumptions in discounted cash flow models, which drives higher current valuations.

Can a business moat disappear?

Yes. Moats are not permanent. Technological shifts, regulatory changes, and evolving consumer preferences can erode even the strongest structural advantages. Morningstar and other analysts regularly downgrade moat ratings when competitive conditions change materially.